%20(4).png)

Contact

Find us

- RCK Partners,

70 Gracechurch Street,

London,

EC3V 0HR.

© 2024 RCK Partners - Company House No: 12396021

Very few owners of Build-to-Rent properties (BTR) and Purpose-Built Student Accommodations (PBSA) are aware of the potential tax savings that can be claimed for the development, renovation, or acquisition of their properties by way of Capital Allowances.

Capital Allowances are a form of tax relief for capitalised expenditure of commercial property. When a commercial property is built, refurbished, or acquired, a portion of that expenditure is eligible for Capital Allowances. These allowances can be deducted from a business’ profits, thus lowering a business' tax liability.

Capital Allowances are eligible for various entities such as, limited companies, partnerships, and sole traders. The following 4 conditions must be met by businesses seeking to claim Capital Allowances on the assets within their business:

· The business must be a UK tax-paying entity.

· The business must have incurred capital expenditure in acquiring the asset.

· The asset must be used as part of the business’ trade.

· The business must hold a relevant interest in the land (such as a freehold or a leasehold).

In general, Capital Allowances are subject to a dwelling restriction which has been imposed by HMRC. This means that purely residential Assured Shorthold Tenancy Agreements (ASTs) and long-term rentals are not eligible to claim Capital Allowances, regardless of the business’ operating trade.

However, Capital Allowance legislation and prior case law have set precedent for the ability to claim capital allowances for the non-dwelling areas of BTR and PBSA by claiming on the communal areas of the properties. This is great news for owners of BTR and PBSA, as all the plant & machinery fixtures within the communal areas suddenly become eligible for additional tax relief. This includes fixtures such as lifts, electrics, lighting, ventilation, fire alarm systems, and a whole lot more.

Unlike accountants and auditors, Capital Allowance specialists have deep expertise within the real estate sector. Our RICS chartered surveyors combined with the expertise of our tax specialists means that the amount of tax relief that your business may be eligible for will be maximised, whilst staying in-line with HMRC guidelines and legislation.

Seeking the expertise of a Capital Allowance specialist is crucial, as our team will be able to effectively quantify the expenditure that relates to the communal areas of the building, utilising a combination of detailed floor plans, comprehensive site surveys, and market research.

Depending on the size and nature of the build / renovations of BTR and PBSA, the tax savings will naturally vary on a case-by-case basis. Generally, up to 35% of these costs will qualify for Capital Allowances, by utilising many avenues of allowances such as Annual Investment Allowances, Writing Down Allowances, and Full Expensing.

For example, if a business incurred £10 million of capital expenditure for the build of a PBSA, up to 35% of this expenditure could qualify for Capital Allowances, which equates to £3.5m of eligible capital expenditure.

At a 25% corporation tax rate, this would equate to £875k of tax savings to be realised throughout the business overtime.

The good news is that Capital Allowances can be claimed retrospectively, no matter how long ago the expenditure was incurred. This is conditional on the fact that the assets are still used within the business and have not been replaced since.

However, the timing of claiming Capital Allowances has a big impact on the timeframe in which the tax savings are realised. For instance, to maximise the tax savings which are received upfront, it is best to make use of the Annual Investment Allowance and Full Expensing, for which the expenditure needs to have been incurred in the last 2 open tax periods. If this deadline has been missed, the total relief available will not change, however these savings will be received overtime instead, thus ameliorating your business’ cashflow for the next several years.

If you believe that any of the above may be relevant to your business, it is strongly advised to get in touch with a Capital Allowance specialist, such as the team at RCK Partners, who can accurately quantify the tax savings available for your business.

If you have any question regarding Capital Allowances or whether you think you are eligible, then please do get in touch with us. We only charge a contingency fee ‘on success’, meaning that there is no risk in exploring the opportunity. If there is no saving, you will receive a free accurate evaluation of your Capital Allowances status, and peace of mind knowing that your Capital Allowances are fully optimised.

To learn more visit our dedicated Capital Allowances webpage.

Find out who can claim capital allowances in the UK, and which assets and property types qualify.

A step-by-step guide to making a capital allowance claim in the UK.

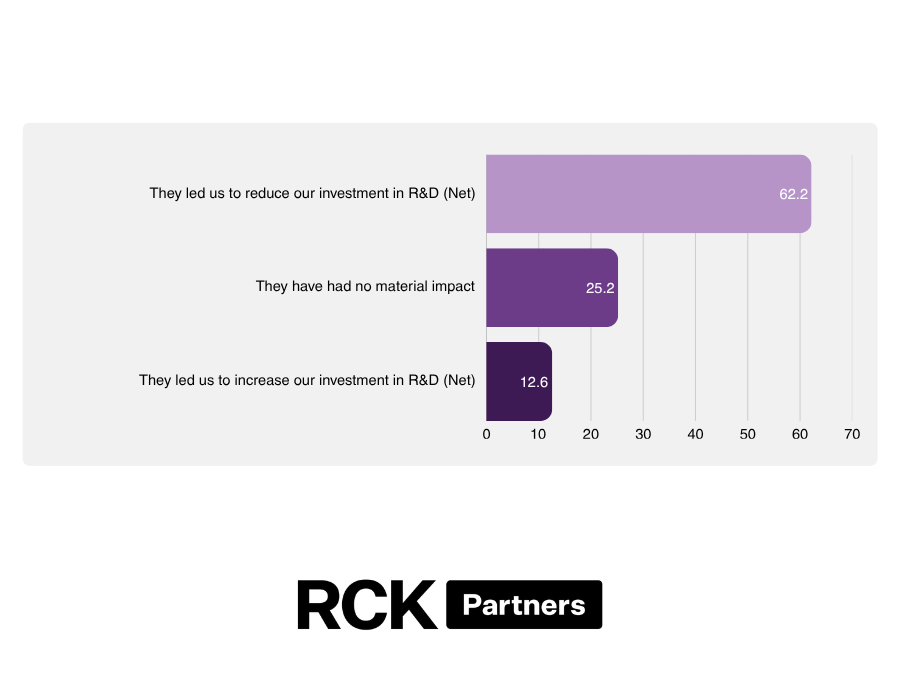

A Times-featured study, commissioned by RCK Partners and conducted by Censuswide, suggests that recent reforms to the UK's R&D tax relief scheme may have gone too far. The research found that measures introduced by HMRC to tackle abuse of the scheme are having unintended consequences for genuine innovators, with many businesses reporting that they have cancelled research initiatives, paused investment plans and reduced skilled headcount as a result of increased uncertainty surrounding the regime.