.png)

.jpg)

Contact

Find us

- RCK Partners,

70 Gracechurch Street,

London,

EC3V 0HR.

© 2024 RCK Partners - Company House No: 12396021

.png)

We sat down with Anastasiya Kokonova MRICS, Capital Allowances Partner at RCK Partners, to explore a key capital allowance: Writing Down Allowances (WDA).

While some capital allowances provide immediate relief, such as the Annual Investment Allowance (AIA) or Full Expensing, when claiming WDA, not all qualifying expenditure can be relieved in the year it is incurred. Writing Down Allowances allow businesses to claim tax relief gradually over time on qualifying plant and machinery expenditure that has not been fully relieved under other allowances.

In practice, WDAs apply to many types of capital expenditure, including fixtures within commercial property, equipment, and long-life assets. Understanding how WDAs work is particularly important for businesses undertaking property acquisitions, refurbishments, or capital investment projects where expenditure exceeds the AIA limit or does not qualify for first-year relief.

Anastasiya is a Chartered Quantity Surveyor with 16 years of experience in the Capital Allowances sector. Prior to specialising in Capital Allowances, Anastasiya worked as a Quantity Surveyor for 3 years at a large QS firm,gaining experience in both new-build and fit-out projects. Anastasiya has provided Capital Allowances advice and undertaken claims on hundreds ofproperties and commercial transactions, and has advised a wide variety of property investors across sectors, including high-net-worth individuals, hoteliers, retailers, media, investment companies, and owner-occupiers. Anastasiya holds a Masters Degree in Corporate Real Estate Finance and Strategy.

Writing Down Allowances allow businesses to claim tax reliefon qualifying capital expenditure over time where the cost has not been fully relieved under Annual Investment Allowance (AIA) or other first-year allowances.

Qualifying expenditure is allocated to capital allowance “pools”, and a percentage of the remaining balance is deducted each year on a reducing balance basis.

The main difference is that AIA provides 100% tax relief inthe year the expenditure is incurred, whereas Writing Down Allowances provide tax relief gradually over time. AIA must be claimed in the year of expenditure, while WDAs can also apply to historical expenditure where AIA or other first-year allowances could not be or were not claimed.

Currently, 18% for the main pool (reducing to 14% in April 2026) and 6% for the special rate pool.

WDAs are calculated on a reducing balance basis so that tax relief is spread over the useful life of the asset. They also apply where expenditure does not qualify for Full Expensing (for example where assets are second-hand) or where AIA cannot be claimed because the annual limit has been exceeded or the claim is out of time.

Capital allowance pools group together qualifying assets (for example the main pool or special rate pool). The relevant WDA percentageis then applied to the remaining balance of each pool each year.

Assets such as integral features within buildings (e.g.electrical systems, lighting, heating, lifts and air-conditioning), long-lifeassets and certain thermal insulation.

Long-life assets (typically with an expected useful life of 25 years or more) are allocated to the special rate pool and attract WDAs at the lower rate.

Yes. Integral features within commercial property generally qualify for capital allowances and are allocated to the special rate pool. If they do not qualify for AIA or first-year allowances, relief can be claimed through Writing Down Allowances.

The relevant WDA percentage is applied to the tax written down value of the relevant capital allowance pool at the end of each accounting period on a reducing balance basis.

Yes, WDAs can be claimed annually until the balance of thepool is fully relieved.

Full Expensing provides 100% first-year relief for qualifying new plant andmachinery for companies. If expenditure does not qualify for Full Expensing (for example because the asset is not new), or if the claim is out of time as Full Expensing must be claimed in the year of expenditure, the cost can instead be claimed through Writing Down Allowances so the entitlement to tax relief is not lost.

Fixtures within commercial properties are relieved through Writing Down Allowances where other allowances such as AIA or first-year allowances are notavailable.

Writing Down Allowances continue to play an important role in helping UK businesses obtain tax relief on capital expenditure that cannot be claimed under AIA or other first-year allowances. By providing relief overtime, WDAs ensure that businesses can still benefit from capital allowances ona wide range of qualifying assets.

We encourage businesses to start a conversation around Writing Down Allowances and whether they are being fully utilised. At RCK Partners, we would be happy to support further discussions around how WDAs andother capital allowances may apply.

For more information or to continue the conversation, click here.

%20(454%20x%20297%20px)%20(33).png)

Yes - commercial property is one of the most significant areas for capital allowances claims in the UK. When a business acquires, constructs, or refurbishes a commercial property, qualifying plant and machinery embedded within it (heating, ventilation, electrical, and cold water systems) is eligible for capital allowance relief.

This is sometimes referred to as embedded capital allowances or fixtures and fittings tax relief: assets that are physically part of the building rather than freestanding items.

Capital allowances on commercial property are particularly valuable because embedded assets are often not recorded in standard accounting records. A capital allowances survey can identify significant unclaimed relief on items that have been in place since the building was acquired.

When purchasing a second-hand commercial property, a Section 198 election must be agreed between buyer and seller within two years of completion. Failure to do so can permanently remove the buyer's right to claim. Getting specialist advice before you exchange contracts is strongly recommended.

Yes. Capital expenditure on refurbishing or renovating a commercial property can qualify, provided the work goes beyond routine maintenance. Qualifying expenditure typically includes:

Routine repairs, like restoring an asset to its original condition without improvement, are revenue expenditure and cannot be claimed as capital allowances.

Yes. Capital allowances on investment property can be claimed by property investors subject to UK income tax or corporation tax, provided the property is commercial and the investor is the legal owner. Getting specialist advice before you exchange contracts is strongly recommended. As with any commercial property purchase, the Section 198 election window closes two years after completion, so this needs to be on the agenda from day one.

Capital allowances cannot generally be claimed on residential rental property. The Furnished Holiday Lettings (FHL) regime, which previously allowed capital allowances on certain short-term residential lets, was abolished from April 2025.

For commercial rental property (offices, retail units, industrial units), the commercial landlord can claim capital allowances on qualifying plant and machinery including embedded fixtures, provided they are the legal owner and the expenditure has been properly pooled.

Yes, in many cases. If you are a leaseholder and have incurred capital expenditure on improving a leasehold property for business use, for example, fitting out a leased office, you may be able to claim capital allowances on those improvements, even without owning the freehold. The qualifying expenditure must meet the plant and machinery tests under the Capital Allowances Act 2001. Specialist advice is recommended.

Capital Allowances are generally not available on residential dwellings, including buy-to-let properties and Houses in Multiple Occupation (HMOs).

Until April 2025, an exception existed for Furnished Holiday Lettings (FHLs), where qualifying expenditure could attract Capital Allowances. Following the abolition of the FHL regime from April 2025, no new Capital Allowances claims can generally be made on expenditure incurred on FHL properties. However, any existing Capital Allowances pool balances can continue to attract writing down allowances in the normal way.

That said, Capital Allowances opportunities do exist for certain residential investment properties, particularly Built to Rent (BTR) developments and purpose-built residential schemes. Whilst Capital Allowances are generally not available on the individual residential units, they may be available on qualifying communal areas and shared facilities, including reception areas, residents' lounges, gyms, co-working spaces, cinema rooms, lifts, plant rooms, lighting, heating and cooling systems, CCTV, access control systems and other qualifying plant and machinery.

As the rules are complex and depend on the type of residential property and its use, specialist Capital Allowances advice should always be sought to determine whether a claim is available and to maximise any available tax relief.

Commercial landlords can claim capital allowances on qualifying plant and machinery embedded within their properties, provided they are taxpaying entities and the expenditure has been correctly pooled. This applies to both freehold and long leasehold owners. Residential landlords are generally not eligible following the abolition of the FHL regime.

Property developers can claim capital allowances on plant and machinery used in development activities. Expenditure on the buildings themselves is generally treated as trading stock where properties are developed for sale. Where a developer retains completed buildings for commercial letting, capital allowances on embedded fixtures may be available. The line between trading and investment activity is not always straightforward, so specialist advice is worth taking before making a claim.

Yes, but cars are subject to specific rules. Cars are excluded from AIA and Full Expensing and use Writing Down Allowances instead, with the rate determined by CO2 emissions:

Sole traders must restrict the claim to the business-use proportion and maintain a mileage log.

Yes. New and unused zero-emission (fully electric) cars qualify for a 100% first-year allowance, available to both companies and unincorporated businesses until March/April 2027. Second-hand electric cars do not qualify for the 100% allowance but enter the main rate pool for WDA at 14% per year.

The rate for hybrid cars depends on CO2 emissions. Plug-in hybrids at 50g/km or below enter the main rate pool at 14% per year; hybrids above 50g/km enter the special rate pool at 6%. No hybrid qualifies for the 100% first-year allowance.

Yes. Vans are treated as plant and machinery rather than cars, provided they meet HMRC's definition of a van. They qualify for the Annual Investment Allowance — the full cost can be deducted in the year of purchase up to the £1 million AIA limit. Sole traders must restrict the claim to the business-use proportion where the van is also used privately.

For sole traders in particular, the AIA provides a straightforward route to tax relief on a van purchase in the year it is bought.

Car writing down allowances are the way businesses claim tax relief on cars over time. Cars are excluded from AIA and Full Expensing, so the cost enters the relevant pool and a percentage is deducted each year on a reducing balance basis. For example: a car costing £30,000 in the main rate pool attracts WDA of £4,200 in year one (14% × £30,000), then £3,612 in year two (14% × £25,800 remaining), and so on until sold or scrapped.

The opportunity lies in identifying qualifying plant and machinery embedded within commercial buildings — HVAC systems, electrical installations, lifts, fitted kitchens, cold water systems — that are often not recorded in standard accounting. These can represent a significant proportion of the property value and a substantial unclaimed tax saving. A capital allowances survey can quantify this - get in touch with RCK to see how we can help.

The timeline depends on the complexity of the claim and the quality of available records. For straightforward plant and machinery claims, relief can be included in the current year's tax return with minimal delay. For commercial property claims involving a full survey, the process typically takes six to twelve weeks from initial review to a completed report ready for HMRC submission.

Plant and machinery allowances (PMAs) cover assets that perform a function within the business: equipment, machinery, and embedded fixtures such as heating and electrical systems. The Structures and Buildings Allowance (SBA) covers expenditure on non-residential building construction or renovation, including walls, roofs, and floors, at 3% per year. The two reliefs are complementary and can be claimed on the same project.

Yes. Law firms can claim capital allowances on qualifying capital expenditure incurred in their trade, including office fit-out costs, IT equipment, and telecoms. A capital allowances survey can often identify significant unclaimed relief on embedded fixtures not captured in the firm's asset register.

Every business is different, and eligibility depends on the nature of the expenditure, how assets are owned, and how they are used in the trade. Get in touch with RCK Partners to find out whether a claim is viable and what it could be worth.

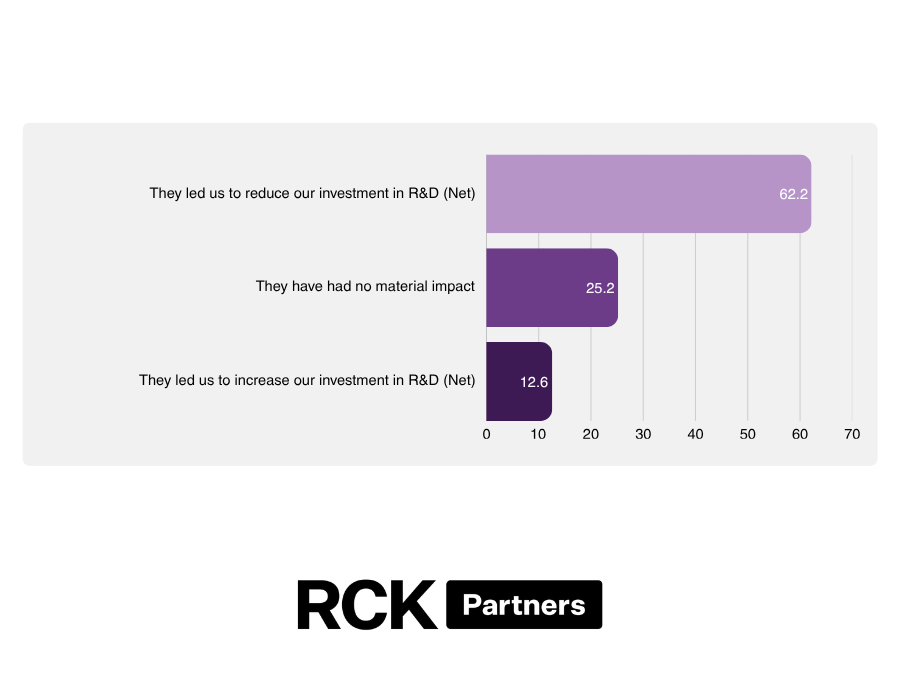

A Times-featured study, commissioned by RCK Partners and conducted by Censuswide, suggests that recent reforms to the UK's R&D tax relief scheme may have gone too far. The research found that measures introduced by HMRC to tackle abuse of the scheme are having unintended consequences for genuine innovators, with many businesses reporting that they have cancelled research initiatives, paused investment plans and reduced skilled headcount as a result of increased uncertainty surrounding the regime.

Capital allowances are the main form of UK tax relief that allows businesses and property owners to deduct the cost of qualifying capital assets from their taxable profits. Governed by the Capital Allowances Act 2001, they take the place of commercial depreciation and provide a structured mechanism for obtaining relief on capital expenditure, either upfront or over time.

Capital allowances on cars allow UK businesses to claim tax relief on the cost of vehicles used for business purposes. This guide is written by RCK Partners to help UK businesses understand capital allowance claims on vehicles.