.png)

.jpg)

Contact

Find us

- RCK Partners,

70 Gracechurch Street,

London,

EC3V 0HR.

© 2024 RCK Partners - Company House No: 12396021

Innovation in the defence sector differs from that in many other industries. Projects are often developed within highly secure environments, where sensitive technical information cannot be shared and confidentiality is critical.

UK defence companies claiming R&D tax credits face unique compliance challenges and this complexity is exactly why many defence businesses either avoid claiming R&D tax credits in entirety, or submit claims that are later enquired by HMRC due to a lack of supporting evidence.

In our experience at RCK Partners, the problem is rarely that the work itself is ineligible. More often, claims fail because businesses struggle to translate highly technical and sensitive defence activity into a format that satisfies HMRC’s evidence expectations and thresholds without compromising sensitive company and project information.

The reality is that defence companies are often undertaking some of the UK’s most advanced qualifying R&D projects and should not be deterred from claiming. This is why specialist defence-sector expertise matters when claiming R&D tax credits.

This guide walks through the most common compliance risks in defence R&D Tax Relief claims and how businesses can structure claims for sensitive projects to satisfy HMRCs requirements and to withstand their scrutiny.

For companies operating within the defence and dual-technology sectors, the challenge is often not whether qualifying R&D exists, it is whether the claim has been structured in a way that satisfies HMRC’s criteria.

Because defence projects are typically complex, sensitive, and highly technical, claims can quickly run into issues if evidence is not substantiated correctly. This is why we advise working with a R&D tax credit agent who has a bespoke defence team, such as RCK Partners, who have security cleared personnel and can translate this sensitive information into a format which satisfies HMRC's requirements.

Below are the areas where we most commonly see defence-sector claims encounter problems during HMRC reviews.

One of the biggest compliance risks is misunderstanding what actually qualifies as R&D for tax purposes.

Many defence businesses assume that because a project is technically advanced, bespoke, or linked to national security, it automatically qualifies. However, HMRC’s definition of R&D focuses on whether the company attempted to resolve scientific or technological uncertainty.

This is particularly important in defence environments where projects often involve a mixture of:

HMRC expects businesses to demonstrate:

To summarise, a company must be trying to achieve something that the wider field didn't know how to effectively do at the outset and which couldn't be readily worked out by a competent professional using information which is publicly available.

Defence-sector claims can be scrutinised because projects operate within secure or classified environments where documentation can be fragmented or insufficient.

As a result, key information is often omitted from the R&D report or Additional Information Form (AIF) by either the company or its provider. To address this, RCK Partners offers guidance to ensure that the developments undertaken are communicated in line with HMRC guidance and expectations, helping to mitigate risk within the submission.

The main evidence issue that we see is that detailed records are kept but due to the sensitive nature of the data, some clients are hesitant in disclosing this information.

We as a specialist defence R&D tax credit provider, are well placed to handle this evidence, involving appropriately security cleared personnel where necessary, to translate this into a format which doesn't compromise this information, yet satisfies HMRCs requirements to successfully award the credit.

In defence environments, claims need to be prepared carefully to balance HMRC requirements with security obligations. This is where specialist advisors with defence-sector experience can make a significant difference.

Subcontracting is one of the most misunderstood areas of UK R&D Tax Relief, particularly within defence supply chains where multiple contractors and specialist providers may be involved. Whether subcontractor costs qualify depends on several factors, including:

Engaging specialist advice ensures these risks are mitigated from the outset for the claiming company.

Project narratives are one of the most important parts of any R&D Tax Relief claim, yet they are also one of the areas where defence companies most commonly encounter difficulties. Since projects are sensitive or classified, businesses often remove too much technical detail from submissions or focus on the unrelated details to the R&D Legislation. The result is narratives that are too vague for HMRC to properly assess the R&D taking place.

For defence businesses, preparing project narratives often requires a careful balance between technical detail, compliance requirements, and security considerations, which is why specialist defence-sector expertise is so important in claim preparation. Importantly, this can still be achieved without disclosing classified or operationally sensitive information when communicated correctly.

RCK Partners operate a layered, 360-degree defence R&D tax credit advisory model including:

Combined, this allows RCK Partners to help defence businesses submit robust, compliant claims while carefully managing confidentiality and security considerations. Read more about RCK’s defence initiative on our dedicated webpage.

At RCK Partners, we believe that a strong process is protection. Please see an outline of our framework for delivering an R&D within the defence sector below:

At RCK Partners, we do not retain classified data on our systems, but instead we work with clients at their locations and on their systems, to access the information that we need in order to prepare a claim with appropriate detail at the right security classification. This ensures that our client’s raw data remains secure, but that the R&D claim meets HMRC requirements for detail.

Defence companies are undertaking some of the most complex and advanced R&D in the UK, yet many claims still fail under HMRC scrutiny.

In most cases, the issue is not eligibility, it is how the claim has been structured, evidenced, and communicated. Balancing HMRC’s requirement for detailed technical evidence with the need to protect sensitive information requires a highly specialised approach.

With the right structure, supporting evidence, and technical narrative, defence-sector claims can be both compliant and robust, without compromising security.

If your business is carrying out innovative work but is uncertain whether your claim would withstand HMRC scrutiny, speaking to an RCK Partners adviser with defence-sector expertise can make the difference between a rejected submission and a successful, defendable claim.

Get in touch to speak with a member of our defence team.

Gajan is a Principal Consultant at RCK Partners, specialising in complex, software-led R&D across VC-backed technology companies, deep-tech start-ups, and dual-use organisations. He leads end-to-end R&D delivery for claims within the technology sector, translating advanced engineering projects into compliant claims that deliver commercial value. Since joining RCK, Gajan has played a key role in building the firm’s software-focused R&D capabilities, enabling the secure onboarding and delivery of work for large multinational and emerging multinational technology companies. More recently, he has helped establish RCK’s dedicated defence and dual-use R&D offering, supporting organisations operating in highly regulated and sensitive industries. Gajan works closely with CTOs, engineers, and founders to coordinate technical inputs, assess system design and technical risk and translate complex engineering work into robust, defensible R&D submissions. To date, he has delivered over 300 R&D claims within the SME, RDEC, ERIS and Merged Schemes.

Albert holds a BEng in Aerospace Engineering (Design) and a MSc in Advanced Motorsport Engineering from Cranfield University. He has industrial experience within the aerospace and automotive sector. Since joining RCK in September 2022 as an Associate R&D consultant, and now an Assistant R&D Manager, he has compiled claims for a range of sectors including defence, agriculture, engineering, oil and gas, and construction. He has an interest in the Engineering sector (defence, aerospace, automotive, marine, motorsport and precision engineering) within the scope of technology and manufacturing developments.

%20(454%20x%20297%20px)%20(33).png)

Yes - commercial property is one of the most significant areas for capital allowances claims in the UK. When a business acquires, constructs, or refurbishes a commercial property, qualifying plant and machinery embedded within it (heating, ventilation, electrical, and cold water systems) is eligible for capital allowance relief.

This is sometimes referred to as embedded capital allowances or fixtures and fittings tax relief: assets that are physically part of the building rather than freestanding items.

Capital allowances on commercial property are particularly valuable because embedded assets are often not recorded in standard accounting records. A capital allowances survey can identify significant unclaimed relief on items that have been in place since the building was acquired.

When purchasing a second-hand commercial property, a Section 198 election must be agreed between buyer and seller within two years of completion. Failure to do so can permanently remove the buyer's right to claim. Getting specialist advice before you exchange contracts is strongly recommended.

Yes. Capital expenditure on refurbishing or renovating a commercial property can qualify, provided the work goes beyond routine maintenance. Qualifying expenditure typically includes:

Routine repairs, like restoring an asset to its original condition without improvement, are revenue expenditure and cannot be claimed as capital allowances.

Yes. Capital allowances on investment property can be claimed by property investors subject to UK income tax or corporation tax, provided the property is commercial and the investor is the legal owner. Getting specialist advice before you exchange contracts is strongly recommended. As with any commercial property purchase, the Section 198 election window closes two years after completion, so this needs to be on the agenda from day one.

Capital allowances cannot generally be claimed on residential rental property. The Furnished Holiday Lettings (FHL) regime, which previously allowed capital allowances on certain short-term residential lets, was abolished from April 2025.

For commercial rental property (offices, retail units, industrial units), the commercial landlord can claim capital allowances on qualifying plant and machinery including embedded fixtures, provided they are the legal owner and the expenditure has been properly pooled.

Yes, in many cases. If you are a leaseholder and have incurred capital expenditure on improving a leasehold property for business use, for example, fitting out a leased office, you may be able to claim capital allowances on those improvements, even without owning the freehold. The qualifying expenditure must meet the plant and machinery tests under the Capital Allowances Act 2001. Specialist advice is recommended.

Capital Allowances are generally not available on residential dwellings, including buy-to-let properties and Houses in Multiple Occupation (HMOs).

Until April 2025, an exception existed for Furnished Holiday Lettings (FHLs), where qualifying expenditure could attract Capital Allowances. Following the abolition of the FHL regime from April 2025, no new Capital Allowances claims can generally be made on expenditure incurred on FHL properties. However, any existing Capital Allowances pool balances can continue to attract writing down allowances in the normal way.

That said, Capital Allowances opportunities do exist for certain residential investment properties, particularly Built to Rent (BTR) developments and purpose-built residential schemes. Whilst Capital Allowances are generally not available on the individual residential units, they may be available on qualifying communal areas and shared facilities, including reception areas, residents' lounges, gyms, co-working spaces, cinema rooms, lifts, plant rooms, lighting, heating and cooling systems, CCTV, access control systems and other qualifying plant and machinery.

As the rules are complex and depend on the type of residential property and its use, specialist Capital Allowances advice should always be sought to determine whether a claim is available and to maximise any available tax relief.

Commercial landlords can claim capital allowances on qualifying plant and machinery embedded within their properties, provided they are taxpaying entities and the expenditure has been correctly pooled. This applies to both freehold and long leasehold owners. Residential landlords are generally not eligible following the abolition of the FHL regime.

Property developers can claim capital allowances on plant and machinery used in development activities. Expenditure on the buildings themselves is generally treated as trading stock where properties are developed for sale. Where a developer retains completed buildings for commercial letting, capital allowances on embedded fixtures may be available. The line between trading and investment activity is not always straightforward, so specialist advice is worth taking before making a claim.

Yes, but cars are subject to specific rules. Cars are excluded from AIA and Full Expensing and use Writing Down Allowances instead, with the rate determined by CO2 emissions:

Sole traders must restrict the claim to the business-use proportion and maintain a mileage log.

Yes. New and unused zero-emission (fully electric) cars qualify for a 100% first-year allowance, available to both companies and unincorporated businesses until March/April 2027. Second-hand electric cars do not qualify for the 100% allowance but enter the main rate pool for WDA at 14% per year.

The rate for hybrid cars depends on CO2 emissions. Plug-in hybrids at 50g/km or below enter the main rate pool at 14% per year; hybrids above 50g/km enter the special rate pool at 6%. No hybrid qualifies for the 100% first-year allowance.

Yes. Vans are treated as plant and machinery rather than cars, provided they meet HMRC's definition of a van. They qualify for the Annual Investment Allowance — the full cost can be deducted in the year of purchase up to the £1 million AIA limit. Sole traders must restrict the claim to the business-use proportion where the van is also used privately.

For sole traders in particular, the AIA provides a straightforward route to tax relief on a van purchase in the year it is bought.

Car writing down allowances are the way businesses claim tax relief on cars over time. Cars are excluded from AIA and Full Expensing, so the cost enters the relevant pool and a percentage is deducted each year on a reducing balance basis. For example: a car costing £30,000 in the main rate pool attracts WDA of £4,200 in year one (14% × £30,000), then £3,612 in year two (14% × £25,800 remaining), and so on until sold or scrapped.

The opportunity lies in identifying qualifying plant and machinery embedded within commercial buildings — HVAC systems, electrical installations, lifts, fitted kitchens, cold water systems — that are often not recorded in standard accounting. These can represent a significant proportion of the property value and a substantial unclaimed tax saving. A capital allowances survey can quantify this - get in touch with RCK to see how we can help.

The timeline depends on the complexity of the claim and the quality of available records. For straightforward plant and machinery claims, relief can be included in the current year's tax return with minimal delay. For commercial property claims involving a full survey, the process typically takes six to twelve weeks from initial review to a completed report ready for HMRC submission.

Plant and machinery allowances (PMAs) cover assets that perform a function within the business: equipment, machinery, and embedded fixtures such as heating and electrical systems. The Structures and Buildings Allowance (SBA) covers expenditure on non-residential building construction or renovation, including walls, roofs, and floors, at 3% per year. The two reliefs are complementary and can be claimed on the same project.

Yes. Law firms can claim capital allowances on qualifying capital expenditure incurred in their trade, including office fit-out costs, IT equipment, and telecoms. A capital allowances survey can often identify significant unclaimed relief on embedded fixtures not captured in the firm's asset register.

Every business is different, and eligibility depends on the nature of the expenditure, how assets are owned, and how they are used in the trade. Get in touch with RCK Partners to find out whether a claim is viable and what it could be worth.

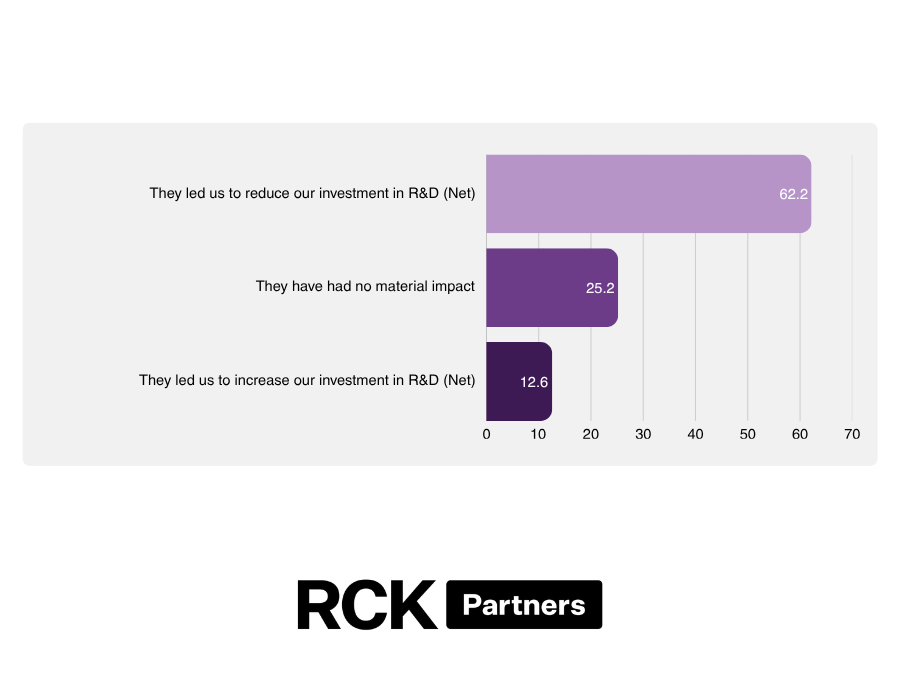

A Times-featured study, commissioned by RCK Partners and conducted by Censuswide, suggests that recent reforms to the UK's R&D tax relief scheme may have gone too far. The research found that measures introduced by HMRC to tackle abuse of the scheme are having unintended consequences for genuine innovators, with many businesses reporting that they have cancelled research initiatives, paused investment plans and reduced skilled headcount as a result of increased uncertainty surrounding the regime.

Capital allowances are the main form of UK tax relief that allows businesses and property owners to deduct the cost of qualifying capital assets from their taxable profits. Governed by the Capital Allowances Act 2001, they take the place of commercial depreciation and provide a structured mechanism for obtaining relief on capital expenditure, either upfront or over time.

Capital allowances on cars allow UK businesses to claim tax relief on the cost of vehicles used for business purposes. This guide is written by RCK Partners to help UK businesses understand capital allowance claims on vehicles.