%20(4).png)

Contact

Find us

- RCK Partners,

70 Gracechurch Street,

London,

EC3V 0HR.

© 2024 RCK Partners - Company House No: 12396021

.jpg)

We spoke with Anastasiya Kokonova, Capital Allowances Partner at RCK Partners, to break down one of the most valuable reliefs currently available to UK businesses: first year allowances. With the introduction of measures such as full expensing and the 100% first year allowance, FYAs have become a powerful tool for accelerating tax relief on qualifying capital expenditure.

For businesses investing in plant and machinery, understanding what is first year allowance and how to apply it correctly can have a significant impact on cash flow and overall tax efficiency. In this Q&A, we explore how first year capital allowance rules work, who can benefit, and the key considerations businesses should keep in mind to maximise immediate tax relief.

First year allowances allow businesses to claim an enhanced level of tax relief on qualifying capital expenditure in the year the cost is incurred, rather than spreading relief over several years. In simple terms, if you’re asking what is first year allowance, it is a form of accelerated tax relief.

Depending on the type of asset, this can be up to the 100% first year allowance or 50%, providing an immediate deduction against taxable profits.

First year allowances are generally available to businesses subject to UK tax, but availability depends on the specific relief. For example, full expensing and the 50% first-year allowance are only available to companies within the charge to corporation tax.

Unlike the Annual Investment Allowance (AIA), first year allowances such as full expensing and the 50% allowance are not subject to an annual monetary cap. However, they are restricted to qualifying expenditure and specific conditions.

Assets that form part of the building structure, such as walls, floors, and roofs, are excluded. Land, residential property, and certain other assets like cars (depending on emissions) are also typically excluded or subject to different rules.

Qualifying assets include new and unused plant and machinery, such as equipment, fixtures, and certain building systems.

Main pool assets may qualify for the 100% first year allowance under full expensing, while special rate assets (e.g. integral features) may qualify for the 50% first-year allowance.

The key benefit of the 100% first year allowance is accelerated tax relief. Businesses can deduct the full cost of qualifying assets from their taxable profits immediately, improving cash flow and reducing corporation tax liabilities in the year of investment.

There are restrictions depending on the type of first year capital allowance. Full expensing and the 50% allowance are only available to companies, must relate to new and unused assets, and generally exclude assets acquired for leasing.

First year allowances such as full expensing and the 50% allowance apply only to new and unused assets. Second-hand assets typically qualify for relief through AIA or writing down allowances instead.

Historically, enhanced capital allowances (ECAs) provided 100% first-year relief for energy-efficient equipment. While most ECA schemes have been withdrawn, certain targeted reliefs still exist.

This includes areas such as first year allowances on electric cars, where qualifying zero-emission vehicles may still benefit from favourable treatment under specific rules.

Yes. Different types of expenditure within the same project can attract different allowances. For example, some assets may qualify for AIA, others for first year allowances, and the remainder for writing down allowances.

However, the same expenditure cannot be claimed under more than one relief.

Common mistakes include claiming on ineligible assets, failing to identify qualifying expenditure, overlooking restrictions (such as leasing or second-hand assets), and not timing the claim correctly within the accounting period.

Businesses should maintain detailed cost records, review expenditure carefully, and seek specialist advice where needed. A structured capital allowances review can ensure qualifying assets are correctly identified and that the most beneficial first year capital allowance treatment is applied.

First year allowances offer a valuable opportunity for businesses to accelerate tax relief and improve cash flow, particularly in periods of significant investment.

However, with varying rules, eligibility criteria, and interactions with other allowances, it’s essential to apply first year allowances correctly to achieve the full benefit. By understanding what is first year allowance and how FYAs fit within the wider capital allowances framework, businesses can make more informed investment decisions and avoid missing out on available reliefs.

If you’re planning capital investment or want to ensure you’re making the most of the reliefs available, speaking with a specialist can help you identify opportunities, avoid common pitfalls, and optimise your claims with confidence. Get in touch here.

Find out who can claim capital allowances in the UK, and which assets and property types qualify.

A step-by-step guide to making a capital allowance claim in the UK.

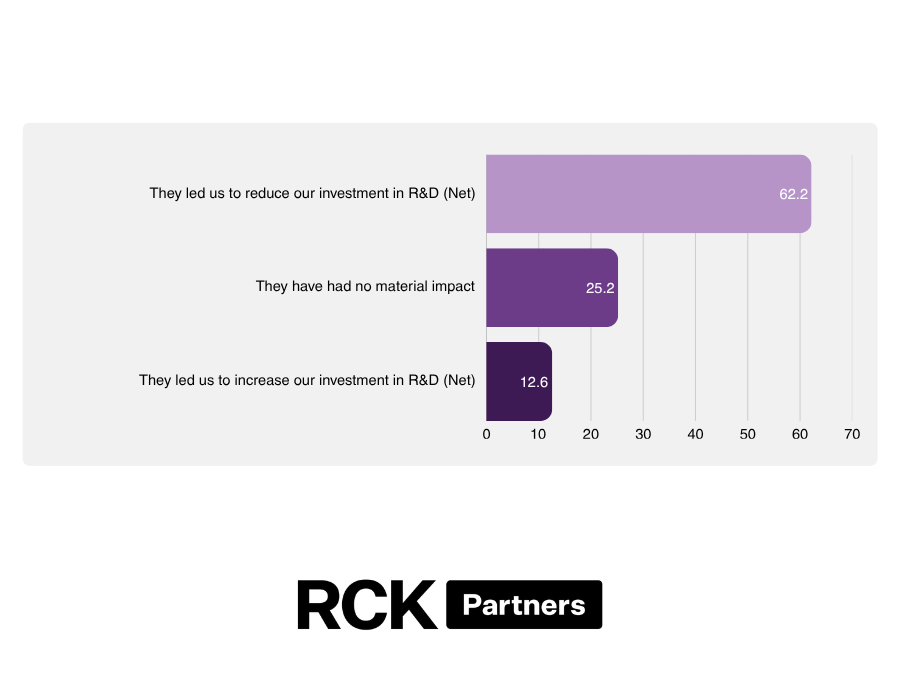

A Times-featured study, commissioned by RCK Partners and conducted by Censuswide, suggests that recent reforms to the UK's R&D tax relief scheme may have gone too far. The research found that measures introduced by HMRC to tackle abuse of the scheme are having unintended consequences for genuine innovators, with many businesses reporting that they have cancelled research initiatives, paused investment plans and reduced skilled headcount as a result of increased uncertainty surrounding the regime.