%20(4).png)

Contact

Find us

- RCK Partners,

70 Gracechurch Street,

London,

EC3V 0HR.

© 2024 RCK Partners - Company House No: 12396021

.webp)

As a former Research and Development (R&D) Tax inspector for HMRC, compliance was at the forefront of my mind when I made the decision to join RCK partners as a HMRC Liaison officer, within the Compliance team.

Compliance within the R&D tax relief scheme has never been more important, with the results of HMRC’s Mandatory Random Enquiry Programme (MREP), outlining greater levels of error and fraud than previously expected, resulting in a major overhaul in activity to tackle non-compliance. But how did we get here?

The R&D tax relief scheme, inadvertently created a perfect storm that made it attractive to unscrupulous agents, aiming to; at best push the boundaries of qualifying activity, and at worse defraud HMRC out of money that their clients were not entitled to. The factors affecting this behaviour include:

1. The unregulated nature of the R&D tax advice/consulting industry

2. Generous cash incentives available to claimants

3. Limited HMRC investigations

RCK’s approach to compliance can help mitigate these risks and help the right companies to make the right claims and continue to benefit from the scheme which is crucial to supporting investment in innovation within the UK.

The R&D tax industry is, and always has been unregulated. This means that an individual could set up a business today and beyond registering for AML supervision (if not already part of a membership organisation), there are no further requirements before they can start offering their service as an R&D tax advisor. This means that for a lot of R&D tax agents, the same individuals are writing the report, calculating the qualifying expenditure and submitting the claim to HMRC, with little to no internal checks, and often without the industry expertise required to be confident that a claim is eligible and correctly compiled.

This is where RCK’s approach differs:

1) The individuals preparing the claim are consultants with relevant academic qualifications specialising in key industries, including experts in life-sciences, software, architecture and civil engineering (to name only a few!).

2) The consultants are fully tax trained and encouraged to pursue tax qualifications (ATT, CTA) to enable them to correctly identify eligible expenditure and conduct accurate tax work.

3) Thirdly, every claim is fully audited by the Compliance team, with RCK being the first R&D tax specialist to establish an independent compliance function consisting only of qualified accountants, tax professionals, experts in R&D Compliance and ex-HMRC inspectors (I am not the only one), to self-regulate and ensure that every claim being submitted to HMRC is of the highest quality. The Compliance team scrutinise each claim with the tax inspector mindset before it goes out. This includes the claim eligibility and a review of the financial calculations, meaning that the team have all the answers to the questions HMRC might ask. Not only does this reduce the risk of enquiry, but it makes dealing with those that do arise much more efficient.

The R&D tax regime has always offered generous incentives for claimant companies, prior to the rate changes that came into effect for expenditure incurred on or after 1 April 2023, a loss making Small or Medium Enterprise (SME) spending £100k on eligible R&D activities would be entitled to a tax credit payment of £33,350, with the benefit reducing slightly for expenditure incurred after 1 April 2023.

One of the ways that HMRC have sought to tackle non-compliance was the introduction of the merged scheme, coming into effect for accounting periods beginning on or after 1 April 2024, this increased the benefit for a large Company whilst decreasing relief for SME’s.

Under the new scheme, an R&D intensive SME (a SME spending at least 30% of their, and that of any connected companies, relevant expenditure on eligible R&D activity), making a loss, spending £100k on eligible R&D activity would be able to receive a cash payment of £26,970.

The benefit to claiming for a large company has actually increased following the merged scheme, with a payable tax credit of up £16k per £100k of eligible spend.

The scheme still offers generous relief in the form of tax credits for claimant companies, especially when considering that successful R&D projects should help improve the trade of the company going forward.

With so many changes to eligibility and expenditure rules, including the introduction of allowable costs relating to data licences and cloud computing costs, it has never been more important to ensure the claim undergoes the appropriate level of scrutiny to ensure compliance.

At RCK, the R&D consultants are knowledgeable about the new rules, eligible costs and the appropriate methodology used to calculate the claim. The Compliance team offer additional checks regarding the qualifying expenditure included in the claim, including corroborating this data with the accounts and ledgers and other records gathered during the process to ensure the Company is not over claiming. Where eligible costs have been accurately included, but may require additional explanations, the compliance team ensure that these mitigations are included in the HMRC submissions. The role is not only to ensure that the costs claimed, and methodology used make sense and are in line with the latest guidelines, but also to ensure that the company is not missing out on costs that they are entitled to.

Prior to the results of HMRC’s 2020/21, Mandatory Random Enquiry Programme, HMRC were only enquiring into 1% of all submitted claims. With this level of checks, it was inevitable that such a scheme would attract abuse. In order to tackle the levels of error and fraud, HMRC have increased the amount of enquiries undertaken. Although enquiries cannot be completely avoided, as HMRC still conduct random enquiries, it does mean that through the Compliance team reviews, which closely resemble HMRC’s approach to risking cases, we are able to mitigate these risks and achieve an enquiry percentage significantly below the perceived industry average. Because of the work of our specialist consultants and additional checks done by the Compliance team, RCK are confident that the claims submitted to HMRC are in line with the latest legislation and guidance. Because of this, we provide our HMRC enquiry defence as standard and that is where the experienced Enquiry defence team come into play.

Enquiries can be a daunting prospect for any company, understanding your rights, HMRC’s powers and responsibilities, how to present the technical elements of the claim within the boundaries of R&D guidelines and the potential risks at each stage, are vital to the enquiry being successfully concluded. The first thing I do when receiving an enquiry is arrange a meeting with the client, to explain the enquiry process to them and answer any questions that they may have. I then translate the information requests made by HMRC, as often these requests include large lists of records, which are not reasonably required by HMRC to check the accuracy of the return. The opening letter is often the most labour intensive part of the check for the company, as they are required to provide some records to support the claim, after this I gather project information via meetings with the client and RCK do most of the heavy lifting during the enquiry, ensuring each letter is reviewed, signed off and understood by the company before I contact HMRC.

RCK also offer an Enquiry Support Service for external companies under enquiry. This involves a free initial examination of the claim documents and existing enquiry correspondence, a scoping call and risk analysis, and if we believe we can assist you in defending the claim, we can then manage all correspondence with HMRC on your behalf including multiple letter exchanges and potential calls with the inspector. To learn more about our enquiry resolution service visit our dedicated webpage.

If you want to take advantage of the robust Compliance and claim security offered through using RCK Partners, get in touch.

The process will consist of:

· An introductory call: A conversation to understand if you are eligible for R&D tax relief.

· Collection of technical information to support your claim.

· Technical analysis to determine how the claim meets the criteria outlined in the DSIT guidelines.

· Claim reviewed by our Compliance team.

· Finalised package to be submitted to HMRC - this will include the technical and financial aspects of the R&D tax claim and filing of additional information form by RCK (AIF).

· HMRC’s stated aim is to pay 85% of payable tax credits within 90 days.

In conclusion, the R&D tax relief scheme is here to stay, and eligible companies should not be put off from claiming. However, compliance has never been more important, and a claimant company should have this at the forefront of their minds when choosing an R&D advisor to represent them.

Find out who can claim capital allowances in the UK, and which assets and property types qualify.

A step-by-step guide to making a capital allowance claim in the UK.

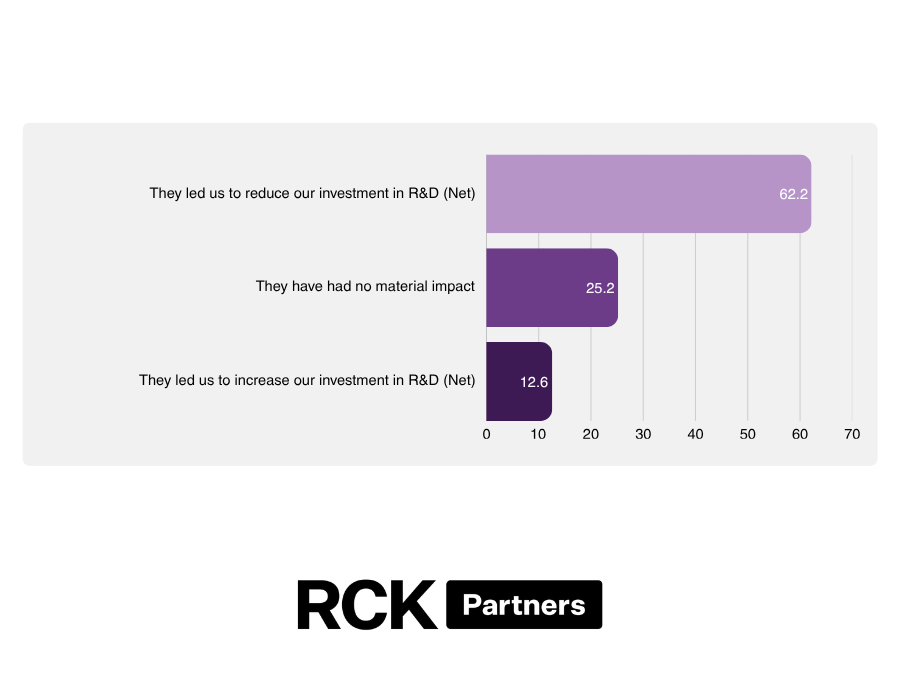

A Times-featured study, commissioned by RCK Partners and conducted by Censuswide, suggests that recent reforms to the UK's R&D tax relief scheme may have gone too far. The research found that measures introduced by HMRC to tackle abuse of the scheme are having unintended consequences for genuine innovators, with many businesses reporting that they have cancelled research initiatives, paused investment plans and reduced skilled headcount as a result of increased uncertainty surrounding the regime.