%20(4).png)

Contact

Find us

- RCK Partners,

70 Gracechurch Street,

London,

EC3V 0HR.

© 2024 RCK Partners - Company House No: 12396021

.jpg)

We spoke with Anastasiya Kokonova, a Capital Allowances Partner at RCK Partners, to explore the treatment of integral features in commercial property and how they can provide tax relief for UK businesses.

Integral features are a key consideration for businesses looking to maximise Capital Allowances on commercial property. These building systems, ranging from electrical and HVAC systems, to lifts and solar shading, can represent a significant portion of expenditure in acquisitions and refurbishments. Recognising these features and understanding the reliefs available can help businesses accelerate tax savings and enhance overall investment efficiency.

Anastasiya is a Chartered Quantity Surveyor with 15 years of experience in the Capital Allowances sector. Prior to specialising in Capital Allowances, Anastasiya worked as a Quantity Surveyor for 3 years for a large QS firm where she has gained experience in both new build and fit out projects. Anastasiya has provided Capital Allowances advice and undertaken claims on hundreds of properties and commercial transactions and has advised a wide variety of property investors across different sectors including high net-worth individuals, hoteliers, retailers, media and investment companies and owner occupiers. Anastasiya holds a Masters Degree in Corporate Real Estate Finance and Strategy.

1. How would you define integral features in the context of Capital Allowances, and why were they introduced in 2008?

Integral features are specific building systems defined in legislation, including electrical systems, cold water systems, heating, ventilation and air conditioning systems, lifts, escalators and external solar shading. They were introduced in 2008 to standardise the treatment of these assets, which previously required detailed analysis to determine whether they were plant or part of the building. The rules now automatically treat these items as plant, but at a reduced rate of relief.

2. What types of assets typically fall within the integral features category, and are there any common misconceptions about what qualifies?

Only assets explicitly listed in legislation qualify as integral features. These include electrical and lighting systems, cold watersystems, HVAC systems (including ducting and certain floors/ ceilings forming part of those systems), lifts and solar shading. A common misconception is that all building-related items qualify; however, elements such as walls, floors andceilings are excluded unless they form an active part of a qualifying system (e.g. a plenum ceiling used for air circulation).

3. How do integral features differ from general plant and machinery for Capital Allowances purposes?

Integral features are treated as plant by statute but are inherently part of the building’s infrastructure. In contrast, general plantand machinery typically perform a direct operational or trading function. The distinction is important because integral features are subject to different pooling rules and rates of relief.

4. Why are integral features usually allocated to the special rate pool, and how does the 6% WDA impact the pace of tax relief?

Expenditure on integral features is classified as “special rate expenditure” and allocated to the special rate pool under the Capital Allowances Act 2001. This attracts writing down allowances at 6%, reflecting their longer economic life and closer link to the building. As a result, tax relief is obtained more slowly compared to main pool assets.

5. In what situations can the Annual Investment Allowance(AIA) or first-year allowances be used for integral features, and how can this accelerate tax relief?

The Annual Investment Allowance (AIA) can be used to claim 100% relief on integral features up to the annual limit in the period the expenditure is incurred. In addition, companies can claim a 50% first-year allowance on new and unused integral features where AIA is not utilised. First-year allowances must be claimed in the period the expenditure is incurred, similar to AIA. These reliefs significantly accelerate tax recovery compared to the standard 6% writing down allowance.

6. What are the key challenges in identifying integral features within a property purchase or refurbishment project?

Integral features are often embedded within wider construction costs and are not separately identified in financial records,making them difficult to isolate without detailed analysis. A comprehensive breakdown of demolition and construction costs is essential to accurately identify qualifying elements. In property acquisitions, additional complexity arises in establishing the ownership and tax history of the property, as this can impact the extent to which integral features can be claimed.

7. How can a detailed Capital Allowances review uncover “hidden” integral features and add value for property owners?

A detailed review can break down construction or acquisition costs and identify qualifying systems that may otherwise be overlooked. This includes analysing mechanical and electrical specifications, contractor costplans and site layouts to isolate integral features within larger projects, often resulting in increased qualifying expenditure and improved tax efficiency.

8. What role do integral features play in large-scale refurbishments compared to property acquisitions?

In refurbishments, a significant proportion of expenditure often relates to the installation or replacement of integral features, making them a key component of the claim. In property acquisitions, integral featurescan also represent a valuable element of the claim, particularly where historical expenditure has not been fully identified or analysed, and where additional qualifying elements can be brought into the claim through a detailed review.

9. Are there any recent legislative or practical changesthat have affected how integral features are treated?

While the definition of integral features has remained largely unchanged, recent changes to Capital Allowances have increased thei mportance of identifying them correctly. The introduction of AIA at higher thresholds and the availability of the 50% first-year allowance means there is greater opportunity to accelerate relief on what would otherwise be special rate expenditure.

10. What practical advice would you give to property owners or advisers to ensure they maximise relief on integral features?

Ensure detailed cost information is retained, engage Capital Allowances specialists early, and review both acquisitions and refurbishments carefully. Particular attention should be given to mechanical and electrical systems, as these often represent a significant proportion of qualifying expenditure but are frequently overlooked without a structured review.

Conclusion

Integral features represent a key area where UK businesses can claim Capital Allowances, particularly in property acquisitions and refurbishment projects. These are often embedded within wider construction costs but are critical to claiming available relief.

Engaging Capital Allowances specialists early, retaining detailed cost information, and understanding the interaction with the Annual Investment Allowance and first-year allowances are critical to maximising relief. At RCK Partners, we support businesses in identifying integral features and ensuring they receive the full benefit of available tax reliefs.

For more information or to discuss how integral featurescould impact your property investments, click here.

Find out who can claim capital allowances in the UK, and which assets and property types qualify.

A step-by-step guide to making a capital allowance claim in the UK.

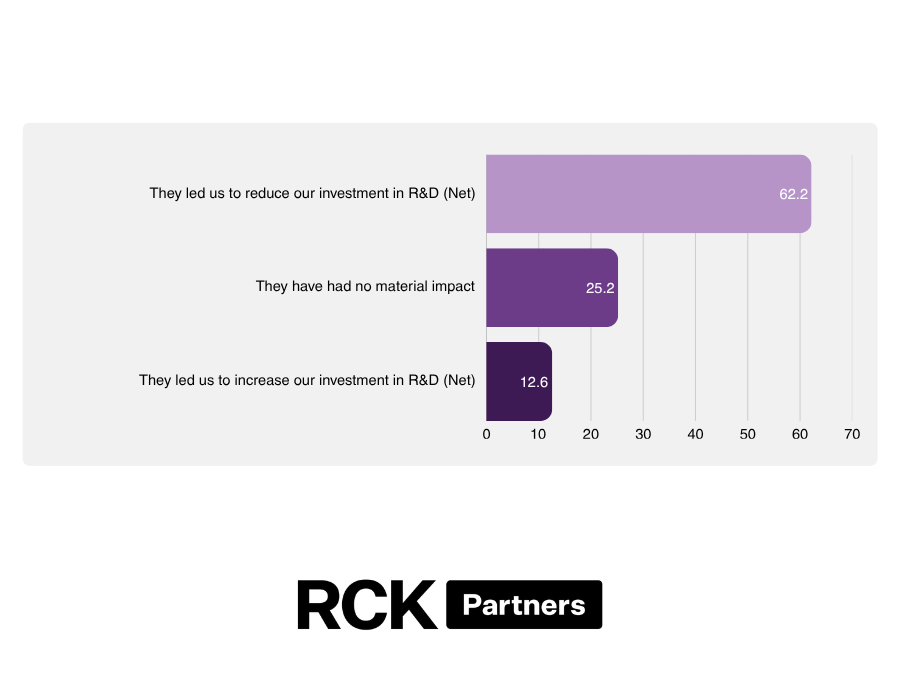

A Times-featured study, commissioned by RCK Partners and conducted by Censuswide, suggests that recent reforms to the UK's R&D tax relief scheme may have gone too far. The research found that measures introduced by HMRC to tackle abuse of the scheme are having unintended consequences for genuine innovators, with many businesses reporting that they have cancelled research initiatives, paused investment plans and reduced skilled headcount as a result of increased uncertainty surrounding the regime.