%20(4).png)

Contact

Find us

- RCK Partners,

70 Gracechurch Street,

London,

EC3V 0HR.

© 2024 RCK Partners - Company House No: 12396021

.png)

The R&D Communication Forum (RDCF) is an annual meeting between HMRC and R&D tax credit agents, serving as a platform for discussing the Research and Development (R&D) tax relief scheme. The forum allows HMRC to communicate upcoming changes, provide operational updates, and answer questions from agents and the public. Each year, detailed notes are released following the session.

The session that took place yesterday covered a wide range of policy, operational, and compliance developments affecting R&D tax credit claims.

2. Policy Update – Guidance and Northern Ireland

Mariam and David presented a number of legislative clarifications regarding the Finance Bill and the application of the overseas expenditure restriction.

Finance Bill clarification:

State Aid Reporting Requirements (Northern Ireland):

From January 2026, claimants in Northern Ireland must comply with new State Aid reporting requirements. Minor changes have been introduced to the Additional Information Form (AIF) to support this.

Typographical Errors in the AIF:

At the previous RDCF, HMRC advised that it would accept agent representations where typographical errors occurred in Unique Taxpayer References (UTRs) in Additional Information Forms (AIFs).

Going forward, HMRC will accept representations for errors involving:

This applies in circumstances whereby the claim would otherwise be valid if not for the typo error. The easement covers both the AIF and the Claim Notification Form (CNF), and the CIRD guidance will be updated accordingly. In the interim period, agents can contact the R&D rights of representation mailbox.

3. ERIS state Aid reporting requirements for the NI and Advanced Assurance (AA) pilot

The forum also covered developments relating to ERIS State Aid reporting and the AA pilot.

AA Pilot:

The Advanced Assurance (AA) pilot's criteria have been extended and are now available for all SMEs. Under the pilot, companies can seek assurance on up to two of the following criteria:

The pilot will go live in May, with guidance to be published shortly. HMRC noted that while they will aim to respond promptly, this will be difficult, and they may limit participation numbers accordingly.

ERIS state Aid reporting requirements for the Northern Ireland:

Companies in NI may claim ERIS for overseas expenditure.

Claimants must:

The AIF was updated in July 2025 to accommodate these requirements.

Notably, there appeared to be some inconsistency in the presentation: while it was stated that overseas expenditure restrictions apply to Northern Ireland ERIS claimants, the slides indicated that ERIS can be claimed for overseas expenditure. This point is expected to be clarified in the final RDCF notes.

Calculating state aid:

When considering the state aid amount from ERIS, it should be calculated as the difference between what would be eligible under the Merged scheme and ERIS. Additionally, the EU has introduced the eAIR register, a centralised system for recording State Aid and de minimis aid that will be publicly available.

4. Compliance Update

HMRC provided several operational updates regarding compliance activity and enquiry handling.

Claim trends:

HMRC reported that:

HMRC stated it continues to meet its processing targets during peak times.

Improvements to customer communication:

HMRC is working to improve the management of customer-facing mailboxes, focusing on:

Currently, there is joint responsibility for this via compliance and operational teams. Actions are taken, but this is sometimes communicated through generic letter responses rather than bespoke emails. HMRC expects improvements to be visible from April onwards.

Further changes are also planned to enable more direct communication with customers and agents, particularly in cases where HMRC intends to open an enquiry but has not yet formally done so. The date of implementation for this is TBC.

Alternative Dispute Resolution (ADR):

Demand for ADR has reduced:

Discontinuation of Campaigns and Projects (C&P):

A major structural change discussed during the forum was the C&P team standing down. The Campaigns and Projects team follows a volume-based approach to compliance checks, so taxpayers do not have a named point of contact throughout an enquiry.

Key points include:

From a practical perspective:

The shift reflects the evolving risk landscape:

5. AI Updates

HMRC discussed both the internal use of AI and the expectations for agents' use of AI.

HMRC’s Use of AI:

All R&D caseworkers now have access to Microsoft Co-Pilot.

However, HMRC emphasised that:

If agents believe that letters or decisions appear to be entirely AI-generated, HMRC encourages them to raise this.

This is in line with the government’s AI roadmap, and this frees up staff time to focus on compliance work.

R&D Summary tool:

HMRC has also tested an AI-powered R&D summary tool that can summarise key information from an R&D report or an AIF. The tool provides caseworkers with a high-level overview of the claim before reviewing detailed information. HMRC emphasised that this is in line with AI ethics guidelines.

During a pilot, testing has so far been limited to cases where casework had already been completed.

The intention is to:

HMRC confirmed it will take a cautious approach before wider rollout.

AI use by agents:

HMRC has published general guidance on the use of software in submissions to HMRC. Agents using AI tools must:

6. Agent registration

HMRC confirmed the upcoming introduction of Tax Adviser Registration, designed to raise standards and tackle non-compliance within the sector. HMRC note that there will be no formal regulation at this time.

Key details include:

7. HM Treasury update

HM Treasury confirmed that its key priorities are:

Feedback from key stakeholders on entrepreneurship highlighted the importance of R&D incentives for start-ups and venture capital investment, reinforcing the government’s focus on maintaining a stable R&D tax environment after a period of policy change.

At RCK, we will continue to closely monitor any changes and ensure our clients are informed of them and how they will affect their claims.

Find out who can claim capital allowances in the UK, and which assets and property types qualify.

A step-by-step guide to making a capital allowance claim in the UK.

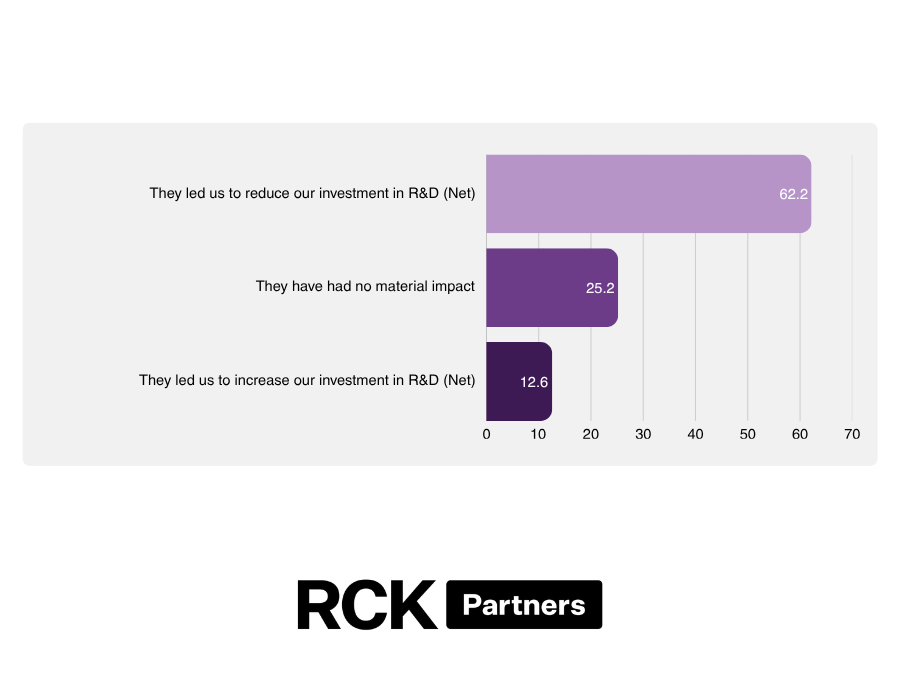

A Times-featured study, commissioned by RCK Partners and conducted by Censuswide, suggests that recent reforms to the UK's R&D tax relief scheme may have gone too far. The research found that measures introduced by HMRC to tackle abuse of the scheme are having unintended consequences for genuine innovators, with many businesses reporting that they have cancelled research initiatives, paused investment plans and reduced skilled headcount as a result of increased uncertainty surrounding the regime.